Dental Insurance – The Australian Guide

We all know that a visit to see the Dentist can be expensive.

The pain you feel pulling your money out of your pocket may seem like a bigger pain than the one that you feel coming from your mouth.

One simple way to lower those costs is to ensure that you have a good dental insurance plan.

5 Dental Insurance topics I will cover in this post

- The difference between minor and major dental, and how to know what you should choose

- What you could be eligible for under the public health care system

- How you can save on gap-fees and prevent waiting periods

- The most important things to look for in an insurance policy

- How to make sure you make the most of your dental insurance

Dental Insurance – So how do you find the right one for you?

If you’re young, healthy, with a good dental history and your teeth are still in great condition, all you probably need is a couple of good professional cleans a year to ensure they stay that way, so a basic policy should do you just fine.

However, if you have any damage, decay, missing teeth, or are needing any major procedures performed, you might be walking straight into the very complicated world known as “major dental”.

If you start contemplating major dental, I want you to know that you should read the fine print behind the policy very carefully.

Every insurer is different, and every policy is structured in a different way.

One fund may be offering a combined limit – where there is one limit that covers all of your extras. Another fund may have set limits for each extra’s category – one for dental, one for physiotherapy, one for chiropractic, and so on.

Sometimes, you may see that each type of treatment within a category will have their own benefit limits – for example, within dental there will be one for general dental, one for major dental, one for endodontics, and one for orthodontics.

The insurance policy you choose will also have a major impact on;

- Your out-of-pocket expenses (also known as your gap-fee)

- Your waiting periods

- The monthly costs you can expect to pay

Confused much yet?!

So today I well be telling you all about how you can make sense of the policies and ensure you get the right one for you, your teeth, and your finances.

I’ve included quite a lot of information in this post, so it is quite a long read.

If you already have a lot of knowledge of the health insurance system, you may prefer to look at the Table of Contents below and skip directly through to any section you want to read.

However, dental insurance can be quite a complex set-up to get a grasp of, so I do recommend that you read all the way from start to finish.

TABLE OF CONTENTS

1. What is dental insurance?

2. How does dental insurance work?

3. What does dental insurance cover?

4. What is the difference between minor dental and major dental?

5. Why are these costs not covered by our public health care system?

6. How much does dental insurance cost?

7. What about other out-of-pocket expenses – will I still need to pay gap fees?

8. What are waiting periods, and do they apply to my dental insurance?

9. What are the most important things to consider when I look for dental insurance cover?

10. How do I make sure I get the most from my dental insurance cover?

11. What are discount dental plans?

12. Where can I find dental insurance

13. Dental insurance – The List

14. Conclusion

What is Dental Insurance?

Dental insurance is an additional extra that you can choose to have as part of your private health insurance – you will see it in the funds’ extras policies, rather than the hospital policies.

If you are taking out private health insurance, you really should look into the funds’ dental insurance policies to make sure it covers everything that you require from dental work – both now and in the long-term.

It’s a very important part of your benefits, as Medicare does not cover much dental work at all, and you and I both know that visiting the Dentist can be a very expensive procedure – one that actually holds back a lot of people from visiting their Dentist.

Not visiting your Dentist for regular check-ups twice yearly can be severely bad for your dental health.

A good dental health policy will cover at least a large portion of the costs of the procedures you require, which is not only better for your oral health, but much better for your finances too!

How Does Dental Insurance Work?

When you visit your Dentist, they will perform an oral examination and diagnose your case.

Then they will create a care plan that outlines your recommended course of treatment.

This plan will include;

- The treatments required

- The costs of the treatments

- How much your insurance is estimated to cover

You will then know the percentage of the treatment – or what is more commonly known as your gap fee – that is not covered by your insurance.

This remaining amount is what is left over for you to pay.

Routine dental work

This includes periodic oral examinations, x-rays, scale and cleans, fluoride treatments, mouthguards and fillings.

All this work is considered preventative treatments, to ensure your teeth stay healthy.

Surgical tooth extraction

If a tooth cannot be saved through treatment due to decay, disease or severe damage, your dental insurance can pay for it to be removed.

Treatment of existing problems with your teeth, and post-operative maintenance

If your teeth are not healthy but can be saved through treatment, your dental insurance will cover some of the costs of major dental work such as root canals, crowns, bridges or dentures, and the post-operative maintenance that is required from these surgeries.

Orthodontics

Your dental insurance plan may also cover some of the costs of work performed by a specialist Dentist, such as braces.

It also covers the ongoing maintenance they require such as retainers.

Emergency dental work

Your dental insurance plan can offer you protection if you unexpectedly damage your teeth in an accident or by receiving a blow to your face, and need your dental work done, like, ASAP.

This is fabulous if you need that work performed urgently but can’t afford the funds upfront.

What is the Difference between Minor Dental and Major Dental?

When it comes to insurance policies, you have the option to choose between a basic or comprehensive level of dental cover.

Your choice will not only make a massive difference on what you pay, but also on the types of procedures for which you are covered.

The main two types of dental policies are;

General Dental

This is the most basic policy, and it only covers common procedures that are generally thought of as protective treatments for your teeth.

They include check-ups, teeth cleanings, fluoride treatments, x-rays and small fillings.

A general check-up at the Dentist

This level of cover is best for those who are young, single and healthy, and have a good, uncomplicated dental history.

I suggest you choose this level of cover if your teeth are in good condition and you know you will only require minor dental treatments, both now and in the long-term.

Major Dental

Major dental is a more comprehensive level of cover, generally covered under the higher level of extras cover, and includes surgery and emergency dental procedures.

As such, it costs more, but also covers you for a lot more procedures.

Major dental basically includes everything that is needed to fix damaged, decayed or missing teeth, even including complicated and expensive procedures like braces, crowns, wisdom teeth removal, bridges, and treatment for gum disease (periodontics).

Major Dental – Implants and Bridge work

You can also receive cover for orthodontic works performed by specialists, and endodontic works like root canals.

If you want a level of cover for both yourself and your family, are a little older and have noticed that your teeth have started to age, or your teeth are just not in a good condition, I suggest you choose major dental cover.

Why are these Costs not Covered by our Public Health Care System?

You will find that Medicare does cover some of the costs of dental work, however, it is limited.

As an adult, Medicare will cover the costs of;

- Dental treatment that is deemed necessary to protect your general health.

- Dental work that is part of a Medicare-approved treatment, such as a dental treatment that is necessary before radiation for oral cancer.

- Any dental work that requires you to be admitted to hospital following the procedure, such as if you have gotten an infection after having a wisdom tooth extracted and need to be hospitalised for treatment.

However, you will find that generally Medicare will not pay for any ongoing maintenance or post-operative treatments that you need once your issue has been rectified.

Nor will they pay any fees for specialists that may have been involved in the treatment, but are seen as not related to your dental condition.

There is also what is known as a Child Dental Schedule Benefits (CDBS), which your child may be eligible for.

To be entitled to receive any of the benefits from the CDBS, your child must be between 2 and 17 years of age during the calendar year.

They also must be eligible for Medicare, and have received a specific payment from the Australian Government such as the Family Tax Benefit A for at least 1 day of the calendar year, meaning you must also meet certain income tests and residence rules.

To see if you apply, visit www.humanservices.gov.au

However, generally you will receive a letter in the mail or online at the beginning of the year advising you if your child meets all the necessary qualifications.

The Child Dental Benefits Schedule is run by the Australian Government and is used every year by roughly 3 million Australian children.

It supplies each eligible child with dental benefits up to $1,000 over a two-year period, by covering either the full costs or part of some of their dental treatments. Dental works that are provided under the CDBS include;

- Oral examinations

- X-rays

- Teeth cleaning

- Fissure sealing

- Fillings

- Tooth extractions

- Root canals

- Partial dentures

It is your choice whether you wish to have your child’s dental services performed in either a public or a private clinic, but there are no benefits provided for dental work performed in a hospital.

Also, no benefits are available for orthodontics or cosmetic dental work.

- Who you are claiming for – That is, whether you are applying for your dental insurance as a single, a couple, a family, or a single parent.

- Your income – The premiums can afford to pay will not only have a say in the level of dental cover you choose, but also the dental cover you are offered. If you earn a high income, it is more possible for you to purchase major dental insurance than for someone who only earns a low income. They instead may be eligible for CDBS or a dental plan.

- Your occupation – Some jobs are more dangerous than others, putting them at a higher risk of any damages to their health and safety, so the cost in which they may have to pay may increase.

- What level of cover you choose – The difference between minor and major dental work will make a difference in your monthly payment, due to the difference in the expenses behind the procedures in which you are allowed to claim.

- The company you choose – Keep your eye on the market, as every company brings out different promotions in order to gain more customers. For example, get the right company at the right time, and you may gain your first two months free!

However, to give you an insight, prices generally range from;

- Single – If you are a single person, you might pay anywhere from $9.14 a month to $347.00 a month

- Couple – A couple can look at paying anywhere from $18.29 a month to $713.60 a month

- Family – A family might choose between paying $18.29 a month or $730.50 a month

- Single Parent – If you are a single parent, you might be up for anywhere between $14.61 a month to $674.20 a month

The general rule of thumb is – the lower the limit, the less you benefit. The higher the annual limits, the more you’ll save.

Some examples are included below to help you wrap your head around this system;

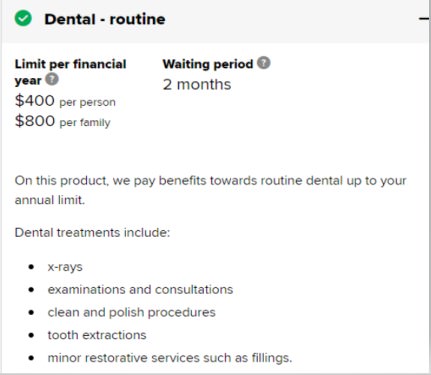

Company – AHM

Minor Dental = $12.85 per month

Waiting Period = 2 Months

Annual Limits = $400 per person, $800 per family

Your cover with AHM minor dental

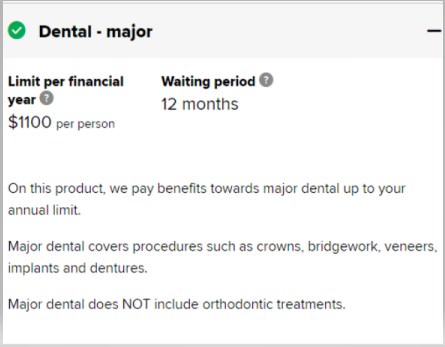

Major Dental = $81.86 per month

Waiting Period = 12 months

Annual Limits = $1000 per person complex dental, $1100 per person major dental, $900 per person orthodontics

Dental – Major. It is always good to check your coverage

- Your out-of-pocket expenses (also known as your gap fee)

- Your benefit limits (the limit you are able to claim on your procedures)

- Your waiting period (how long after you’ve signed up before you can start using your rebates)

Sometimes, the procedure will be covered in full by your insurance provider.

However, there will be other dental treatments where you’ll be charged an out-of-pocket expense, or what is more commonly known as a gap fee.

A good way of knowing what you may be entitled to is to look into the benefit limits of your potential fund and begin to understand what excesses that you may need to pay for procedures.

There will be set limits as to just how much you can claim back on dental treatments on your insurance policy.

Some, such as general dental check-ups, will have no limits. Others will have annual limits – that is, a set amount that you are allowed to claim back over a 12-month period.

For the far more expensive treatments like orthodontics, you’re bound to see a lifetime limit – that is, a set amount you’re allowed to claim back over your entire life – and once you’ve used it up, it’s gone for good.

However, keep your eye out for what is known as a “no gap” dental cover option that many funds are offering!

This is a relatively new policy that has been brought to the market to ensure that you keep your dental health in check – after all, it seems that even the health funds these days don’t like to pay to go to the Dentist!

With the no gap scheme, your health fund will pay all out-of-pocket expenses! Yes, you read that right, they will pay 100% of the costs of your treatment!

These are generally for the preventative dental treatments that will reduce the risk of you developing more serious dental problems later on in life.

Dental treatments that may be covered by a no gap dental cover

- Initial dental check-ups

- Preventative oral examinations

- Scale and cleans

- Topical fluoride treatments

- Basic fillings

- X-rays

- Custom-made mouthguards for sports

Just as it is only available for certain treatments, the other limitation to the gap free dental cover is that you must receive your treatment from a dentist who is in your policy providers network.

But just think – you are spending no money on these Dental visits, so you really cannot complain!

What are Waiting Periods, and do they Apply to my Dental Insurance?

Waiting periods are the length of time that you have to wait until you can use your dental insurance. You will find that they do exist on most policies.

They are a system that is in place to stop you from only taking out your private health insurance if you immediately need an expensive treatment.

You may find some private health insurance companies offer promotions that will let you claim straight away on a service such as general dental – this is a form of marketing in order to attract more members to their health fund.

However, it is highly unlikely that you will find major dental to ever be incorporated in one of these marketing campaigns, simply due to the fact that they are such expensive procedures.

The waiting periods before you can use your rebate on your dental insurance plan are generally;

- General dental – Waiting periods may be relinquished altogether, meaning you can use your dental insure straight away. In other cases, they may be as little as two months.

- Major dental – Waiting periods generally vary anywhere from six to twelve months depending on your funds’ policies and the treatment – this includes even the complex procedures such as endodontics and orthodontics.

What are the Most Important Things to Consider when I look for Dental Insurance Cover?

There are so many factors that you must consider before choosing your level of dental insurance.

Below are the most important questions that you must ask yourself.

By taking all of these factors into account, it will ensure that you get the best dental insurance policy for you and your teeth;

How healthy are your teeth?

If you are not having any issues with your teeth, if they are still in great condition, there is no harm in you choosing a minor policy for a lesser price.

If you foresee yourself needing major dental work done any time in the future or have even had a lot of dental work in the past, this is when you would want to look at getting a policy that covers everything – that is, major dental.

You can still get one of these for under $40 per month, but this $40 or less will save you a fortune when you need the major dental procedures performed.

How old are you?

Not a question many people like to ask, or answer.

But unfortunately, the health of our teeth declines with our age, so, therefore, major dental cover is more popular among those who are just that little bit older and wiser.

How many people are you claiming for?

Everybody with children will tell you that they cost money.

Add the price of dental care on top of the price of children, and you’ve got yourself quite an expense, especially if they require any orthodontic treatment such as braces.

It may offer more protection to you and your finances in the long term to be protected by a higher level of dental cover.

What maximum benefits do you think you will need?

Don’t forget to take into account the benefits limit on each policy.

Once again, if your teeth are in good condition with no major issues, a basic policy might be all you require.

Still, you may want to find one that is going to offer you higher benefit limits.

If you are willing to spend that little bit extra, say $25 a month, rather than $12 a month, the maximum amount of money that you can claim back every 12 months is going to be far higher.

What this means for you is that you will actually spend far less when visiting your Dentist.

How are the benefit limits of the policy structured?

Every single dental policy is going to have a maximum benefits limit, or a maximum amount of money that you can claim on your extras.

However, they are all structured in a different way. Some funds have what is known as a combined limit – this is where there is one limit that covers all of your extras.

In some funds you will see that every extras category will have its own limit (one for dental, one for physiotherapy, one for chiropractic, and so forth).

Sometimes, each type of treatment within a category will have their own benefit limits (for example, within dental there will be one for general dental, one for major dental, one for endodontics, and one for orthodontics).

The policies with combined limits are usually the most beneficial, as what you are able to do is split the benefits to the treatments that you want to receive – you are not limited by the categories.

Does your policy have any unlimited cover and do I need it?

Some policies have no annual benefits limit on certain general dental treatments, such as x-rays and fillings.

If you need a lot of fillings, this would be very beneficial to you.

What exactly is covered in your policy, and what is not?

Make sure you read and understand the fine print – and re-read those Terms & Conditions!

Not all private health insurance policies will cover the same dental treatments, especially for specialist procedures such as orthodontics.

Make sure you know what you’re getting before you get it!

What are the waiting periods?

Most private health insurance companies generally tend to have a waiting period before you can use your insurance benefits.

These vary from two months for general dental to 12 months for major dental and orthodontics.

Are you willing to wait?

If not, keep your eye out on the market for companies offering waiting period promotions. Generally, you will find companies offering no waiting periods on general dental, but it is hard to find companies that offer no waiting periods on major dental.

Are they offering no gap dental?

No-gap dental is a type of dental cover where your insurance provider pays 100% of the cost for certain dental treatments, but only if you use a dentist in their network.

You’ll find in most dental policies the benefit limit covers only a certain percentage of the cost towards your procedure.

For example, your policy might pay 50% of the cost, for major dental work like crowns. You then have to pay the remaining 50%, which is called your gap fee.

However, if you can find a policy that has no-gap dental, there is no gap fee for you to pay!

Go for your routine checkup and clean

You should be owed a twice-yearly scale and clean under your dental plan.

This cleaning is something that you really need to do twice a year, to ensure your teeth remain healthy. And if you’re paying for it, you might as well be using it!

Talk to your Dentist

If you are going for your regular check-ups and your twice-yearly clean like you should be, talk to your Dentist about the condition of your teeth whilst you are there.

Your Dentist will be able to advise you of any work that they think you will need done in the future – whether it be months or years down the line.

Thus, you’ll know if you are going to need any major dental work, and you can upgrade your insurance plan if necessary.

Speaking with your dentist about the condition of your teeth proves to be very helpful

Just remember the waiting periods on every policy – if you time it right, your waiting periods should be finished by the time you are going to need to have the procedures performed.

What are Discount Dental Plans?

If the idea of dental insurance is still overwhelming you, you can always choose a discount dental plan instead.

By taking this option, you will receive discounted prices at the Dentist simply by paying an annual membership fee.

The main advantages of discount dental plans

- Membership fees are relatively low – lower than that of health insurance. Most fees are under $100 a year, even for family cover.

- There are no waiting periods.

- There are no benefit limits or treatment exclusions – you can get discounts on all types of procedures.

The main disadvantages of discount dental plans

- You can’t choose your own Dentist to treat you – you must choose from a network of Dentists that also participate in the scheme.

- Generally, they only cover a lesser percentage of your bill – anywhere from 15% to 40% of your visit.

For those that cannot afford dental insurance or those with healthy teeth, a discount dental plan is worth considering. Some sites you can look at to see whether they are of interest to you are;

Smile

www.smile.com.au

Dentacare

www.dentacare.com.au

Where can I Find Dental Insurance?

There are multiple comparison sites that you can use to compare the costs of dental insurance across Australia. These include;

Members Own

www.membersown.com.au

Finder

www.finder.com.au

iSelect

www.iselect.com.au

Compare the Market

www.comparethemarket.com.au

Health Deal

www.healthdeal.com.au

These sites do a great job of comparing the prices across the market, so you can choose the one that appeals to you.

However, there is only one issue.

Most of the comparison sites will only show you some of the dental insurance options – that is, those of the companies that offer them a commission for referring them.

By using these sites, you will be missing out on plenty of other dental insurance options on the market.

As such, we have compiled a list of every single Dental insurance option available to you across Australia!

You can do the research of options available to you by getting quotations from the below funds (if they are available to you);

| Insurer | Website | Type |

| ACA Health Benefits Funds | https://acahealth.com.au/ | Restricted |

| AHM Health Insurance | https://ahm.com.au/ | Open |

| Australian Unity Health Ltd | https://www.australianunity.com.au/ | Open |

| BUPA HI Pty Ltd | https://www.bupa.com.au/ | Open |

| CBHS Corporate Health Pty Ltd | https://www.cbhscorporatehealth.com.au/ | Open |

| CBHS Health Fund Ltd | https://www.cbhs.com.au/ | Restricted |

| CUA Health Ltd | https://www.cua.com.au/ | Open |

| Defence Health Benefits | https://www.defencehealth.com.au/ | Restricted |

| Doctors’ Health Fund | https://www.doctorshealthfund.com.au/ | Restricted |

| Emergency Services Health | https://eshealth.com.au/ | Restricted |

| Frank Health Insurance | https://www.frankhealthinsurance.com.au/ | Open |

| GMHBA Ltd | https://www.gmhba.com.au/ | Open |

| Grand United Corporate Health | https://www.guhealth.com.au/ | Open |

| HBF Health Ltd | https://www.hbf.com.au/ | Open |

| HCF | https://www.hcf.com.au/ | Open |

| Health Care Insurance Ltd | https://hciltd.com.au/ | Open |

| Health Insurance Fund of Australia Ltd (HIF) | https://www.hif.com.au/ | Open |

| Health Partners | https://www.healthpartners.com.au/ | Open |

| health.com.au | https://health.com.au/ | Open |

| Hunter Health Insurance | https://www.hunterhi.com.au/ | Open |

| Latrobe Health | https://www.latrobehealth.com.au/ | Open |

| Medibank Private Ltd | https://www.medibank.com.au/ | Open |

| Mildura Health Fund | http://www.mildurahealthfund.com.au/ | Open |

| myOwn | https://www.myown.com.au/ | Open |

| Natuinal Health Benefits Australia Pty Ltd (onemedifund) | https://www.onemedifund.com.au/ | Open |

| Navy Health Ltd | https://navyhealth.com.au/ | Restricted |

| nib Health Funds Ltd | https://www.nib.com.au/ | Open |

| NSW Teachers Federation | https://www.nswtf.org.au/ | Restricted |

| Nurses & Midwives Health | https://www.nmhealth.com.au/ | Restricted |

| Peoplecare Health Insurance | https://peoplecare.com.au/Health-insurance/Home/Home | Open |

| Phoenix Health Fund Ltd | https://phoenixhealthfund.com.au/ | Open |

| Police Health | https://policehealth.com.au/ | Restricted |

| Private Healthcare Australia | https://www.privatehealthcareaustralia.org.au/consumers/dental-health-insurance/ | Open |

| Queensland Country Health Fund Ltd | https://www.qldcountryhealth.com.au/ | Open |

| Railway and Transport Health Fund LTD (RT Health Fund) | https://www.rthealthfund.com.au/ | Restricted |

| Reserve Bank Health Society Ltd | https://www.myrbhs.com.au/ | Restricted |

| St Lukes Health | https://www.stlukes.com.au/ | Open |

| Teachers Health | https://www.teachershealth.com.au/ | Restricted |

| Transport Health Pty Ltd | https://transporthealth.com.au/ | Open |

| TUH – Teachers’ Union Health | https://tuh.com.au/ | Restricted |

| Uni Health | https://www.unihealthinsurance.com.au/ | Restricted |

| West Fund Ltd (Western District) | https://www.westfund.com.au/ | Open |

This is a great way to make sure you don’t miss out on the best offers on the market for you and your family!

Conclusion

So by now you should have gained a lot of knowledge of dental insurance.

Remember, it is worth the money – just know what you are spending your money on and get the right policy for you.

If you are young, single and have healthy teeth, a basic dental policy may be all you need – just go for your regular twice-yearly professional cleans, and your Dentist will tell you at any time if this policy needs updating, because they can foresee if you will need any major dental work.

If you are looking for cover for your family, for aging teeth or if your teeth are not in a good condition, it is a wise idea for you to get major dental cover.

Trust me when I say, you’ll thank me for it when you see the benefits you gain back from complex surgeries!

If the whole idea of dental insurance still seems overwhelming or unaffordable, don’t forget to check what you can get through Medibank or through dental plans.

This is always something to consider!

Whatever option you choose – don’t forget to treat that smile of yours with the care it deserves!

By Anthony Cade

Created at July 31, 2019, Updated at January 25, 2025